If you are reading this, you are likely standing at a crossroads. Perhaps a parent has had a fall, or a partner’s needs have suddenly increased, and the phrase “care home” has moved from a distant possibility to an immediate conversation.

Finding the right care is emotional enough without the added stress of deciphering who pays for what. A common misconception is that because we have the NHS, social care is also free. In reality, while the NHS is free at the point of use, social care in the UK is means-tested. This means most families will have to contribute something toward the costs.

This guide breaks down the high-level funding rules for 2025–26, helping you understand where you stand before you sign any contracts.

Key Takeaway: You should never discuss finances until you have agreed on the care needed. Always secure a Needs Assessment first.

How Care Home Funding Works in the UK

Funding care isn’t one‑size‑fits‑all. Broadly, people pay for care in one of three ways:

- Self‑funding: You cover all care costs yourself. If you have significant savings or assets, this may be your situation.

- Local authority support: If your savings and assets fall below set limits, your council may contribute, but only after carrying out official assessments.

- NHS funding: If your needs are primarily health‑related, the NHS may pay for your care under NHS Continuing Healthcare (CHC).

Key Assessments Explained

1: The Needs Assessment (The “What”)

Before you worry about bank accounts or property values, you need to establish exactly what kind of support is required. This is done through a Care Needs Assessment carried out by your local authority social services team.

- It is a statutory right: You are entitled to this assessment regardless of how much money you have.

- It is impartial: The social worker will identify if your loved one needs a residential setting or if their needs can be safely met at home (domiciliary care).

- Why it matters: If the local authority agrees that needs can be met at home, they may not fund a care home place even if you qualify financially. Conversely, if you want care at home, this assessment is the evidence you need to support that choice.

2: The Financial Assessment (The “How Much”)

Once needs are agreed upon, the “means test” begins. This is a financial audit of your loved one’s capital (savings, investments, and potentially property) and income (pensions, benefits).

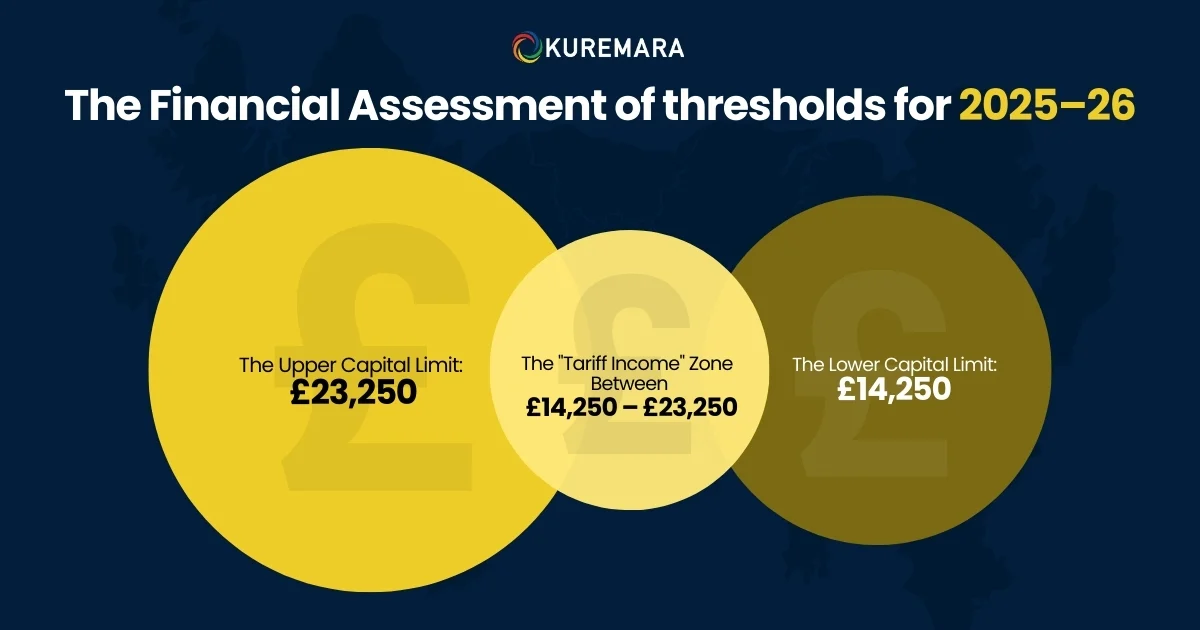

In England, the thresholds for 2025–26 remain fixed at the following levels. These figures determine how much support you can get:

a. The Upper Capital Limit: £23,250

If your loved one has assets above £23,250, they are classed as a “self-funder.”

- They must pay the full cost of their care.

- The “Property” Trap: If they are moving into a residential home permanently, the value of their main home is usually included in this calculation (unless a spouse or dependent still lives there).

b. The Lower Capital Limit: £14,250

If assets are below £14,250, they will receive maximum support from the local authority.

- Note: They will still contribute most of their income (e.g., state pension) toward the fees, keeping only a small “Personal Expenses Allowance” (currently £30.65 per week in England).

c. The “Tariff Income” Zone (Between £14,250 – £23,250)

If assets fall between these two figures, the local authority pays some costs, but the individual must pay a “tariff income”.

- This is calculated as £1 per week for every £250 of capital they have above the lower limit.

Source: nhs.uk

3: When is Care Free? (NHS Support)

Before accepting that you must pay for care, you must ask: Is this a health need?

If your relative’s needs are primarily medical (e.g., complex medication, breathing issues, or terminal illness) rather than social (e.g., washing, dressing), they may qualify for NHS Continuing Healthcare (CHC).

- What it is: A package of care funded 100% by the NHS.

- The Benefit: It is not means-tested. If eligible, the NHS pays for everything: care, accommodation, and food, whether in a nursing home or at home.

The “Consolation Prize”: NHS Funded Nursing Care (FNC)

If you don’t qualify for full CHC but live in a nursing home and need nursing care, the NHS will pay a flat rate directly to the home to cover the nursing portion of the fees.

- 2025–26 Standard Rate (England): The NHS pays £250 per week toward the bill. Make sure this is deducted from the fees quoted to you by the care home.

Important Tip

If you’re self‑funding and think your savings might fall below £23,250 soon, contact your council a few months early for reassessment. Funding only applies from the date the council begins your assessment not retrospectively.

NHS Funding: Continuing Healthcare (CHC)

If the primary reason someone needs care is health‑related, the NHS may cover the full cost under NHS Continuing Healthcare (CHC) and this is not means‑tested. That means income, savings, or assets do not affect eligibility.

CHC is for people with intense, complex, or unpredictable health needs not just social care needs. To qualify, a formal assessment determines whether health needs are the dominant factor.

If someone doesn’t qualify for CHC but still needs registered nursing care in a care home, they may be eligible for NHS‑funded nursing care, where the NHS contributes a fixed amount towards nursing costs.

Regional Differences Across the UK

If your family is outside England, the rules differ significantly:

- Wales: The capital limit is much higher than a single threshold of £50,000. If you have less than this, you can receive support.

- Scotland: Scotland offers Free Personal Care for adults. For 2025–26, the council pays £254.60 per week for personal care and £114.55 per week for nursing care, regardless of your wealth. You only pay for “hotel costs” (accommodation/food) if you have assets.

- Northern Ireland: Health and social care are integrated, but charging rules still apply with a capital upper limit of £23,250.

Understanding where you or your loved one lives helps you navigate the right rules and support available.

Tips for Planning and Avoiding Common Pitfalls

- Start early: Don’t wait until funds run low. Getting assessments started proactively is key.

- Keep documents ready: Collect evidence of income, savings, and assets before assessments.

- Speak up about benefits: Some disability‑related benefits may reduce your assessment contribution.

- Avoid risky “fee‑avoidance” schemes: Transferring assets to get below thresholds can be treated as deprivation by councils.

The “Care at Home” Financial Advantage

At Kuremara, we often help families who are shocked by the cost of residential homes (often £1,200+ per week). It is vital to understand that funding rules treat home care differently.

The Golden Rule: If you receive care in your own home (domiciliary or live-in care), the value of your property is never included in the means test.

- This means your loved one could have a house worth £500,000, but if their liquid savings are under £23,250 (in England), they might still qualify for local authority funding for home care visits.

- This allows your loved one to stay in familiar surroundings while protecting the family inheritance from being sold to pay care home fees.

Conclusion: Clarity, Control, and Confidence with Kuremara

Navigating care home funding doesn’t have to be overwhelming, not when you have the right guidance and support. From understanding assessments to knowing what financial thresholds mean for your family, the first step toward confident decision-making is getting informed.

At Kuremara, we exist to make later-life planning simpler, clearer, and more human. Whether you’re just starting to explore options or facing urgent care decisions, our goal is to give you back a sense of control with information you can trust and real help when you need it.