Families often search for how to avoid care home fees legally during moments of uncertainty. A sudden diagnosis, hospital discharge, or declining health can quickly turn financial concerns into urgent questions. After a lifetime of saving, protecting your home and assets feels entirely natural.

However, there is a critical difference between responsible financial planning and risky asset avoidance. This guide explains what is legally possible, what may raise red flags, and how to approach care decisions in a compliant and informed way.

Why Families Search for Ways to Avoid Care Home Fees

When care becomes a realistic possibility, families commonly worry about:

- Losing the family home

- Depleting lifetime savings

- Reducing inheritance

- Being forced into residential care unnecessarily

Many people are not looking for loopholes. They want clarity. Unfortunately, online advice can blur the line between lawful planning and deliberate deprivation of assets.

Understanding that distinction protects both finances and peace of mind.

How Care Fees Are Assessed in the UK

Before making any financial decisions, it is essential to understand how care funding works.

a. The Care Needs Assessment

The first step is a care needs assessment. This determines whether residential care is required or whether support can be provided at home.

In many cases, individuals may benefit from:

- Structured home care services

- Specialist dementia care

- Live-in care support

- Community-based assistance

Exploring personalised live-in care or structured home care services can sometimes delay or prevent residential placement altogether.

b. The Financial (Means) Assessment

If residential care is required, a financial assessment reviews:

- Savings and investments

- Property ownership

- Income sources

- Trust arrangements

- Past asset transfers

Authorities do not only look at current assets. They may also review financial changes made in recent years to determine whether they were intended to reduce care contributions.

This is where deprivation of assets rules become important.

What Legitimate Care Fee Planning Looks Like

There are lawful, responsible strategies families can consider. The focus should always be on early, transparent planning.

1. Planning Early Before Care Is Foreseeable

Timing is critical.

If financial arrangements are made:

- While in good health

- Without foreseeable care needs

- As part of normal estate planning

- With documented professional advice

They are far less likely to be challenged.

Early planning provides flexibility. Crisis transfers invite scrutiny.

2. Ensuring Assessments Are Thorough and Accurate

Before assuming a care home is necessary, ensure:

- A full care needs assessment has been completed

- NHS Continuing Healthcare eligibility has been explored

- Community-based care options have been reviewed

Sometimes structured care at home provides a safer and more cost-effective solution than immediate residential placement.

3. Exploring Legitimate Funding Support

Depending on circumstances, individuals may qualify for:

- NHS Continuing Healthcare

- Attendance Allowance

- Local authority contributions

- Deferred payment schemes

Understanding these options reduces financial pressure without engaging in risky financial transfers.

4. Seeking Regulated Financial and Legal Advice

Professional guidance is essential.

Qualified advisers can:

- Assess individual risk

- Provide documented recommendations

- Ensure compliance with legal frameworks

- Structure estate planning appropriately

Written advice demonstrates that decisions were made responsibly rather than to deliberately avoid fees.

Understanding Deprivation of Assets

Deprivation of assets occurs when someone deliberately reduces wealth to qualify for financial support.

Local authorities apply several tests.

* The Intent Test

Was avoiding care fees a significant motive behind the transfer?

* The Timing Test

Was care reasonably foreseeable when the asset was transferred?

* The Foreseeability Test

Would a reasonable person have expected care to be required soon?

If deprivation is suspected, authorities may:

- Apply notional capital rules

- Treat transferred assets as still owned

- Refuse financial support

- Recover funds

There is no automatic “seven-year rule.” Transfers may be reviewed whenever intent appears evident.

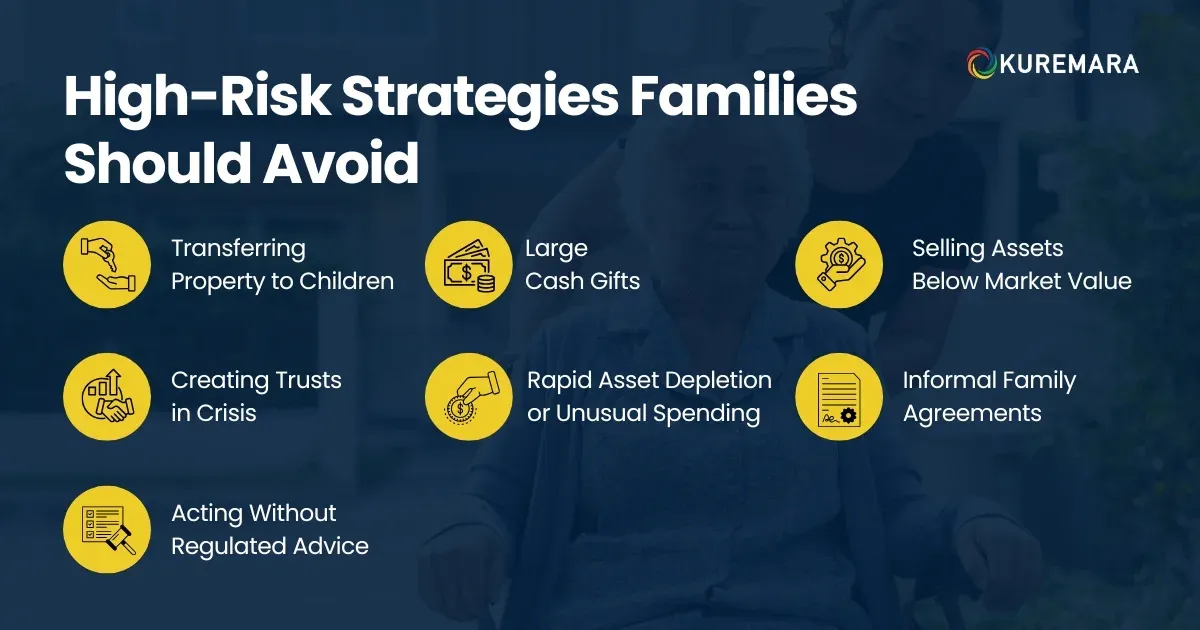

High-Risk Strategies Families Should Avoid

Certain strategies are commonly promoted online as “quick fixes,” but they often carry serious legal and financial risk. Local authorities are experienced in identifying deliberate attempts to reduce assets before assessment. Acting on poor advice can lead to funding refusal, lengthy investigations, and unnecessary family stress.

Short-term solutions may appear attractive in moments of fear, but they frequently create long-term complications.

1. Transferring Property to Children

Signing over your home while health is declining may be treated as deliberate deprivation of assets.

If care needs are already foreseeable, transferring ownership to a child or family member does not automatically protect the property. Local authorities may still treat the home as belonging to you under “notional capital” rules.

Additionally, transferring property creates other risks:

- Loss of control over your own home

- Exposure to your child’s divorce, debt, or bankruptcy

- Potential family disputes

- Capital gains tax implications

What may seem like protection can actually increase vulnerability.

2. Large Cash Gifts

Sudden transfers of savings during illness can trigger investigation.

If gifting occurs when care is reasonably foreseeable, authorities may question whether the intention was to reduce your contribution to fees. Even informal arrangements, such as “helping children out,” may be reviewed if the timing appears connected to declining health.

Gifts that are inconsistent with previous financial behaviour are especially likely to raise concerns.

3. Selling Assets Below Market Value

Undervalue transactions may be reversed or disregarded during financial assessment.

Selling a property or valuable asset to a relative at a discounted price can be interpreted as a deliberate attempt to reduce capital. Authorities assess whether a fair market value was obtained and whether the transaction was commercially reasonable.

If deemed deliberate deprivation, the difference in value may still be counted against you.

4. Creating Trusts in Crisis

Trusts created after diagnosis may be scrutinised closely.

While trusts can form part of legitimate long-term estate planning, establishing one shortly before care is needed may attract attention. Authorities will examine:

- When the trust was created

- The health condition at the time

- The stated purpose of the trust

- Whether avoiding care fees was a motivating factor

Trusts are not automatic shields. Timing and intent matter significantly.

5. Rapid Asset Depletion or Unusual Spending

Large withdrawals, sudden luxury purchases, or transferring funds into unfamiliar accounts may also raise red flags.

Even if money is technically “spent,” authorities may assess whether the spending was reasonable. If it appears designed primarily to reduce assessable capital, it may still be treated as notional capital.

Routine spending aligned with lifestyle is unlikely to cause concern. Dramatic financial changes during declining health often will.

6. Informal Family Agreements

Some families make undocumented arrangements such as:

- “Paying back” children for past support

- Informally assigning assets

- Placing funds in a relative’s account for safekeeping

Without clear legal documentation and consistent long-term history, these actions may be viewed as attempts to shield assets.

Transparency and documentation are critical in any financial arrangement.

7. Acting Without Regulated Advice

Perhaps the greatest risk is acting on unverified online guidance or informal advice.

Financial planning around care fees is highly individual. What works legally for one situation may be inappropriate or risky in another. Decisions made without regulated professional advice are far more likely to be challenged.

Common Myths About Avoiding Care Home Fees

a. “The Council Can Only Look Back Seven Years”

There is no strict time limit if intent can be demonstrated.

b. “Putting the House in My Child’s Name Protects It”

Ownership changes do not override deprivation rules.

c. “Spending Money Quickly Solves the Problem”

Excessive or unreasonable spending may still be treated as notional capital.

Understanding these myths prevents costly mistakes.

Considering Care at Home as a Financial and Emotional Alternative

Residential care is not always the only option.

For many families, personalised home support offers:

- Greater independence

- Familiar surroundings

- One-to-one care

- Emotional stability

Exploring structured live-in care services or tailored domiciliary care support may reduce both emotional stress and immediate financial exposure.

Early conversations around home-based support can significantly change long-term outcomes.

A Safe Decision-Making Checklist

Before making financial changes, ask:

1. Is care reasonably foreseeable?

2. Has a full care needs assessment been completed?

3. Are financial decisions consistent with long-term planning?

4. Have we obtained regulated advice in writing?

5. Could this decision withstand scrutiny?

If uncertainty exists, pause and seek professional advice.

About Kuremara

At Kuremara, we understand that care decisions involve more than finances. As a trusted provider of personalised home care and live-in support across the UK, our focus is on dignity, transparency, and informed choice. We work closely with families to explore safe alternatives to residential placement where appropriate, including structured home care, dementia support, and live-in assistance. Our goal is to help families make confident decisions that prioritise wellbeing while maintaining compliance and long-term stability.

Final Thoughts — Focus on Compliance, Not Loopholes

Searching for how to avoid care home fees legally is often driven by fear. But fear should not guide financial planning.

It is possible to:

- Plan early

- Explore legitimate funding pathways

- Consider care at home options

- Protect assets responsibly

- Seek regulated advice

It is not safe to:

- Hide assets

- Make rushed transfers after diagnosis

- Rely on myths

- Act without professional guidance

Every situation is unique. The safest path is transparent, documented, and professionally supported planning. That approach protects not only your assets but also your peace of mind.